Business

Bank of England in fresh emergency move

The Bank of England has warned of a “material risk” to financial stability as it made a fresh emergency move to try to calm investors.

It said it would buy more government bonds to try to stabilise their price and prevent a sell-off that could put some pension funds at risk of collapse.

It is the third time the Bank has had to step in since the government’s mini-budget sparked alarm among investors.

The chancellor promised huge tax cuts without saying how he would fund them.

The prime minister’s spokesman said she “remained confident” that her plans would boost growth and that she was in regular contact with the Bank.

On Monday, in a bid to reassure investors Chancellor Kwasi Kwarteng said he would bring forward his economic plan where he will spell out how he plans to pay for the tax cuts and provide an independent forecast on the UK economy’s prospects.

Ahead of this the Bank had also said it was prepared to double the amount of bonds it was buying to help support their price, but reiterated it would end this support as planned on Friday.

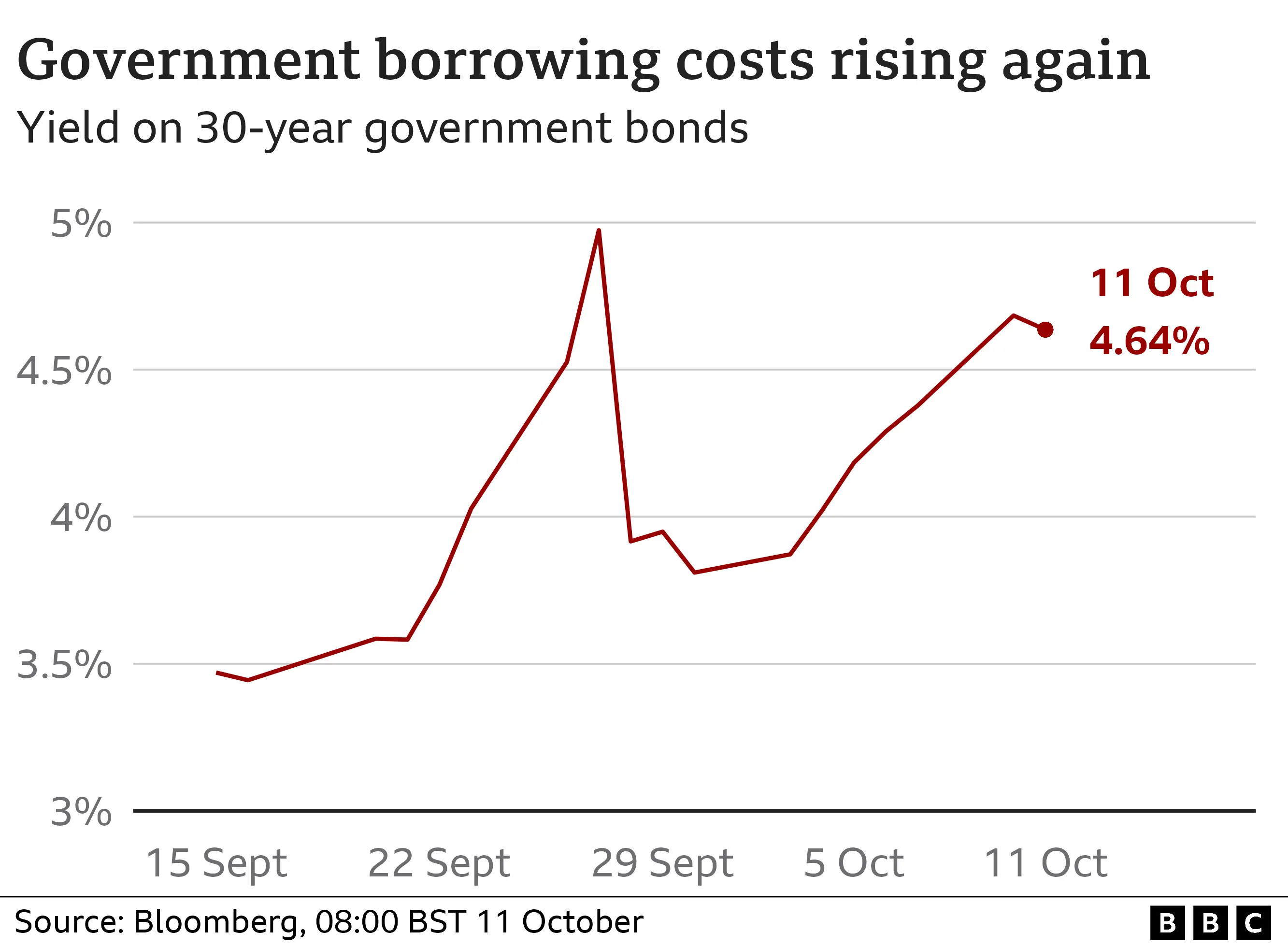

Government borrowing costs rose sharply despite these actions as investors continued to remain wary of buying bonds.

Shadow chief secretary to the Treasury Pat McFadden said the fact the Bank had been forced to step in for a second day running created “renewed pressure for the chancellor to reverse his budget.”

The government raises money it needs for spending by selling bonds to investors. The Bank first stepped in on 28 September, when days after the mini-budget, investors began demanding higher rates of interest on those bonds and government borrowing costs surged to worrying levels.

The market turmoil had forced pension funds to sell bonds due to concerns over their solvency, but this threatened to create a downward spiral in bond prices as more were offloaded and had left some pension funds close to collapse.

By buying bonds, the Bank is hoping to help keep their price stable and prevent investors selling them.

The turmoil has fed through to the mortgage market, where hundreds of products have been suspended due to concerns about how to price these long-term loans.

Last week, interest rates on typical two and five-year fixed rate mortgages topped 6% for the first time in over a decade.

Under pressure from its MPs to change course, the government has been forced into a series of embarrassing climbdowns.

Among other things it had to U-turn on a promise to scrap the top rate of income tax.

On Tuesday, the Institute for Fiscal Studies (IFS) think tank warned that Mr Kwarteng would have to make “big and painful cuts” of up to £60bn to balance the books when he announces his economic plan on 31 October.

Mr Kwarteng will take questions from MPs this afternoon in the Commons for the first time since being appointed.

“A material risk to UK financial stability” are words the Bank of England uses rarely, a warning of a threat to the financial system it can’t confidently ignore. It’s even more rare for several senior Bank executives to have indicated part of the blame for the turmoil may lie at the government’s door, the result of domestic policy.

They’re not alone. The sharp rise in the cost of new government borrowing – the interest on those bonds – reflects an anxiety amongst investors that its tax-cutting plans risk the UK overstretching itself. And it’s pensions funds and borrowers who are hit by the fallout.

It’s the Bank who – again, a rare event – had to try to ease their pain. But it’s made it clear that the medicine is a stop gap – and the lingering unease in the market emphasises it’s ultimately looking to what it sees as the source of its unease – the chancellor’s approach – for a remedy.

Resolving this crisis of faith will ultimately depend on what the chancellor unveils in his Hallowe’en plan. If the IFS is right, the price of restoring credibility could involve upwards of £60bn worth of cuts to public spending.

Explaining its intervention on Tuesday, the Bank of England said government bonds had seen a “significant re-pricing” since the start of the week and warned there was a risk of a fresh downturn in markets.

It said it would now buy a wider range of bonds as well as continue to buy bonds as part of the original emergency measures it launched on 28 September.

Sir John Gieve, a former deputy governor for fiscal stability at the Bank, said the Bank was primarily stepping in to protect pension funds, many of which hold government bonds as investments.

However, he said the “underlying problem” was that markets did not believe the government would be able to cut spending enough before its growth measures took effect.

“The underlying problem came on the back of the announcement of huge amounts of extra borrowing and without a clear plan on how to pay for them,” Sir John told the BBC.

“And the latest speculation on that is that in order to make the books balance [Mr Kwarteng] will have to promise [billions of] spending cuts. It’s one thing to say that, but can he actually deliver that?”

Prime Minister Liz Truss has said that around £43bn of promised tax cuts will boost UK economic growth and therefore pay for themselves.

The chancellor has also committed to publishing an independent forecast of the UK’s economic prospects by the OBR, the independent budget watchdog, at the same time as his economic plan on 31 October – something he declined to do with his mini-budget.

But Ms Truss faces a potential rebellion from her MPs after declining to say whether she would increase benefits in line with inflation next April.

It is thought that increasing benefits in line with wages instead could save the government £5bn.

Reports /TrainViral/

The prospective new owner of Royal Mail has said he will not walk away from the requirement to deliver letters throughout the UK six days a week, as long as he is running the service.

“As long as I’m alive, I completely exclude this,” Czech billionaire Daniel Kretinsky told the BBC.

Mr Kretinsky has had a £3.6bn offer for Royal Mail accepted by its board.

Shareholders are expected to approve the deal in the coming months, but the government also has a say over whether it goes ahead.

Currently the Universal Service Obligation (USO) requires Royal Mail to deliver letters six days a week throughout the country for the same price. But questions have been raised over whether the service could be reduced in the future.

In an exclusive interview with the BBC, Mr Kretinsky also said he would be willing to share profits with employees, if given the go-ahead to buy the group.

However, he appeared to reject the idea of employees having a stake in Royal Mail, which unions have called for in exchange for their support.

The Royal Mail board agreed a £3.6bn takeover offer from Mr Kretinsky in May for the 500-year-old organisation, which employs more than 150,000 people. Including assumed debts, the offer is worth £5bn.

But because Royal Mail is a nationally important company, the government has the power to scrutinise and potentially block the deal.

As well as keeping the new government on side, Mr Kretinsky also faces the task of convincing postal unions that the proposed deal will benefit employees.

The USO is a potential sticking point for both the government and unions.

Royal Mail is required by law to deliver letters six days a week and parcels five days a week to every address in the UK for a fixed price.

How well this has actually been working in practice is a different matter. Ten years ago, 92% of first class post arrived on time. By the end of last year it was down to 74%, according to the regulator Ofcom.

Last year the regulator fined Royal Mail £5.6m for failing to meet its delivery targets.

Royal Mail has been pushing for this obligation to be watered down. It wants to cut second class letter deliveries to every other weekday, saying this will save £300m, and lead to “fewer than 1,000” voluntary redundancies.

‘Unconditional commitment’

Mr Kretinsky has committed in writing to honouring the USO, but only for five years.

And after that, in theory, the new owners could just walk away from it.

However, Mr Kretinsky told the BBC: “As long as I’m alive, I completely exclude this, and I’m sure that anybody that would be my successor would absolutely understand this.

“I say this as an absolutely clear, unconditional commitment: Royal Mail is going to be the provider of Universal Service Obligation in the UK, I would say forever, as long as the service is going to be needed, and as long as we are going to be around.”

Mr Kretinsky added that the written five-year commitment was “the longest commitment that has ever been offered in a situation like this”.

Another potential stumbling block for the deal, however, is how the company will be structured.

Unions would like to see the company renationalised, but Dave Ward, general secretary of the Communication Workers Union (CWU), told the BBC that would be “difficult in the current political and economic environment”.

Instead, what the CWU is pushing for is “a different model of ownership” – that is, where the employees part-own the business.

To get its support for the takeover, the union wants employees to share ownership of the company, along with other concessions including board representation for workers.

It says profit sharing is “not going to be enough to deliver our support and the support of the workforce”.

If the union doesn’t get what it wants, it won’t rule out industrial action, Mr Ward said. Its members went on strike in 2022 and 2023.

Although Mr Kretinsky said he is “very open” to profit sharing, he is not in favour of shared ownership.

“I don’t think the ownership stake is the right model,” he said. “The logic is: share of profit, yes, [but an] ownership structure creates a lot of complexity.

“For instance, what happens if the employee leaves? He has shares, he is leaving, he is not working for the company, he [still] needs remunerating.”

Mr Kretinsky said he didn’t want to create “some anonymous structure” but instead “remunerate the people who are working for the company, and creating value for the company”.

The union is also concerned about job losses and changes to the terms and conditions of postal workers’ contracts.

Mr Kretinsky has guaranteed no compulsory redundancies or changes in terms and conditions but only until 2025.

“If we are more successful, and we have more parcels to be delivered, we need not less people, but we need more people,” he said. “So really, job cuts are not part of our plan at all.”

He said if the management, union and employees work together, “we will be successful”.

Another concern is the potential break-up of the business.

The profit for Royal Mail’s parent company last year was entirely generated by its German and Canadian logistics and parcels business, GLS. Royal Mail itself made a loss.

Mr Kretinsky has promised not to split off GLS or load the parent company with excessive debt, although borrowings will rise if the deal goes through.

But he has a way to go to convince the CWU.

“I can’t think of any other country in the world that would just just hand over its entire postal service to an overseas equity investor,” Mr Ward of the CWU said.

However, Mr Kretinsky said that the postal unions “do understand that we are on the same ship, and that we need this ship to be successful, and that if we are there, we don’t have any real problems to deal with, because the sky is blue, and it’s blue for everybody.”

The union cannot stop this deal but the government can block it under the National Security and Investment Act.

Business Secretary Jonathan Reynolds has said he will scrutinise the assurances and guarantees given and called on Mr Kretinsky to work constructively with the unions.

Mr Kretinsky may say that he and the unions are ultimately on the same ship but, as things stand, they are not on the same page.

Who is Daniel Kretinsky?

Daniel Kretinsky started his career as a lawyer in his hometown of Brno, before moving to Prague.

He then made serious money in Central and Eastern European energy interests.

This includes Eustream, which transports Russian gas via pipelines that run through Ukraine, the Czech Republic and Slovakia.

He then diversified into other investments, including an almost 10% stake in UK supermarket chain Sainsbury’s and a 27% share in Premier League club West Ham United.

The Czech businessman is worth about £6bn, according to reports.

Father of five blasted for leashing kids, gives them odd nickname

This heartwarming prom story goes viral again and we all understand why

Simon Cowell Won’t Leave Son His $600 M Fortune; Says If He or Future Children Wants to “Start a Business … I’ll Invest. They Aren’t Getting Trusts”

Five wedding outfits for just £29!

Mikhail Gorbachev changed history

Tracking the war with Russia

-

Fashion2 years ago

Fashion2 years agoFive wedding outfits for just £29!

-

Politics2 years ago

Politics2 years agoMikhail Gorbachev changed history

-

Politics2 years ago

Politics2 years agoTracking the war with Russia

-

Everything About Youtube2 years ago

Everything About Youtube2 years agoThe Twitter Artist who makes a Fortune off YouTube Thumbnails while Studying.

-

Fashion2 years ago

Fashion2 years agoOn presents first ever shoe made from carbon

-

Politics2 years ago

Politics2 years agoCharles is announced to be the new King

-

Tech2 years ago

Tech2 years agoThe rise of the AI artists stirs debate

-

Everything About Youtube2 years ago

Everything About Youtube2 years agoEveryone knows YouTube, but not how it works.