Business

Bank of England expects UK to fall

The Bank of England has warned the UK is facing its longest recession since records began, as it raised interest rates by the most in 33 years.

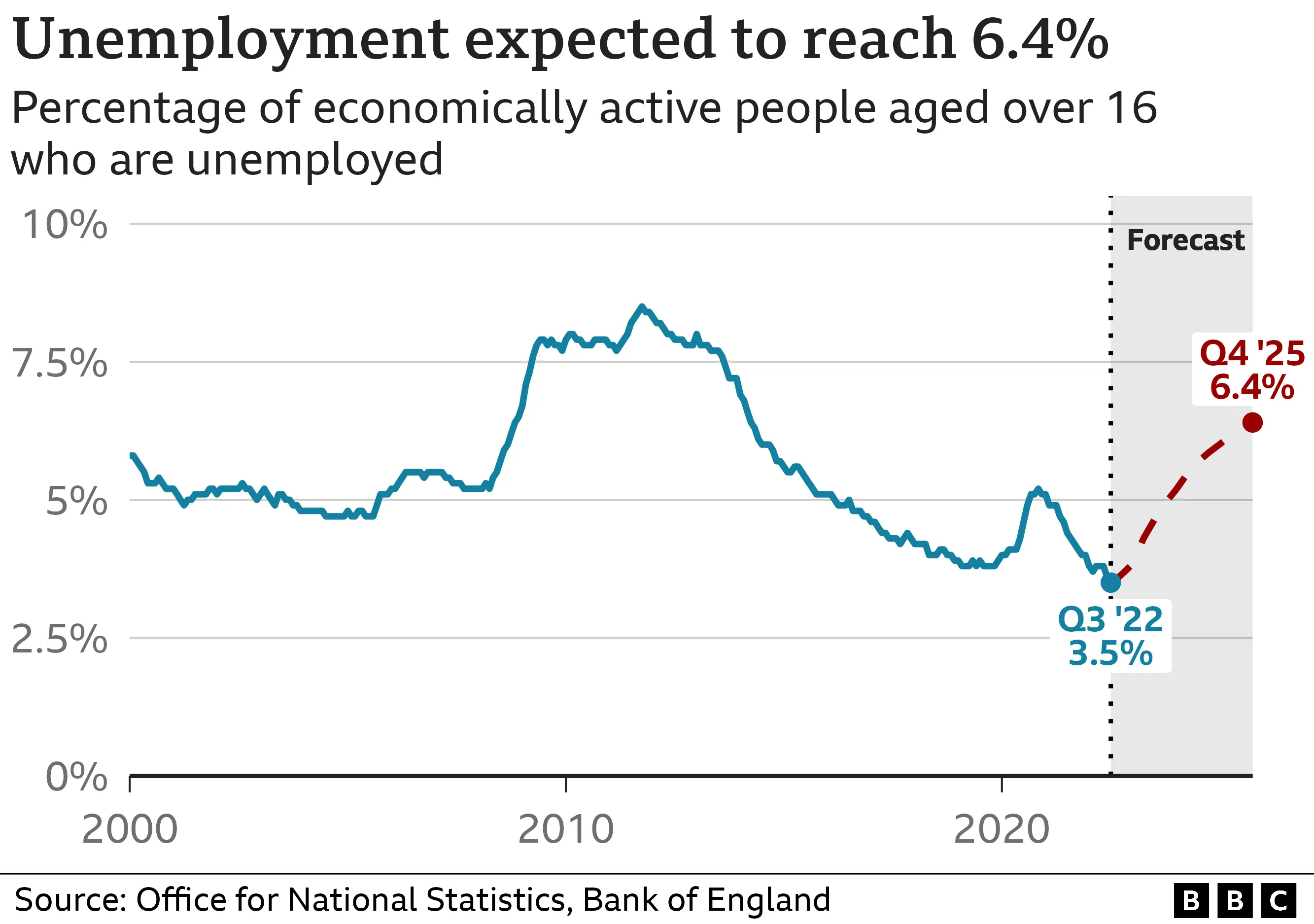

It warned the UK would face a “very challenging” two-year slump with unemployment nearly doubling by 2025.

Bank boss Andrew Bailey warned of a “tough road ahead” for UK households, but said it had to act forcefully now or things “will be worse later on”.

It lifted interest rates to 3% from 2.25%, the biggest jump since 1989.

By raising rates, the Bank is trying to bring down soaring prices as the cost of living rises at its fastest rate in 40 years.

Food and energy prices have jumped, in part because of the Ukraine war, which has left many households facing hardship and started to drag on the economy.

A recession is defined as when a country’s economy shrinks for two three-month periods – or quarters – in a row. Typically, companies make less money, pay falls and unemployment rises. This means the government receives less money in tax to use on public services such as health and education.

The Bank had previously expected the UK to fall into recession at the end of this year and said it would last for all next year.

But it now believes the economy already entered a “challenging” downturn this summer, which will continue next year and into the first half of 2024 – a possible general election year.

While it will not be the UK’s deepest downturn, it will be the longest since records began in the 1920s, the Bank said.

The unemployment rate is currently at its lowest for 50 years, but it is expected to rise to nearly 6.5%.

Chancellor Jeremy Hunt said: “The most important thing the British government can do right now is to restore stability, sort out our public finances, and get debt falling so that interest rate rises are kept as low as possible.”

But shadow chancellor Rachel Reeves said families could not withstand such high rate rises “when we’ve got rising food prices, rising energy bills and now higher mortgage rates as well”.

The latest rate hike – the Bank’s eighth since December – takes borrowing costs to their highest in 14 years, when the UK banking system faced collapse.

The Bank believes by raising interest rates it will make it more expensive to borrow and encourage people not to spend money, easing the pressure on prices in the process.

But while its latest rate rise will be welcomed by savers, it will have a knock-on effect on those with mortgages, credit card debt and bank loans.

‘I’m nervous about the loan on my van’

Michelle, 58, from East Riding in Yorkshire has a loan on a van and is nervous about rising interest rates.

“My disposable income has gone down dramatically recently and I earn more than the amount to get benefits,” she told the BBC. “They need to help the middle earners.”

Michelle needs the van to get to work as there’s no public transport near her. But if her loan repayment costs rise she fears she’ll have to give up the vehicle.

“I can work from home, but like most places my place of work wants us back in the office at least three days a week and I’ve had to have talks with them about how I can afford that.

“It’s a 60-mile round trip, it’s expensive.”

Those with mortgages are also feeling nervous. 43The Bank forecasts that if interest rates continue to rise, those whose fixed rate deals are coming to an end could see their annual payments soar by up to £3,000.

It said that it would increase interest rates if inflation remained high. Financial markets had been expecting rates to peak at 5.25% but the Bank does not expect them to rise this high.

The Bank has done something it doesn’t normally do in the published minutes of its decisions – it has given guidance that seems to suggest a peak in interest rates of about 4.5% next autumn.

For those with a glass half-full – this is lower than the 6% assumed just a month ago in the post mini-budget market turmoil.

While government borrowing costs and the level of the pound has somewhat recovered after a series of U-turns since, mortgage markets and business loans are still showing some stress, adding to the prolonged hit to the economy.

The forecast predicts that the unemployment rate will rise, while household incomes will come down too.

It is a picture of a painful economic period, with the UK performing worse than the US and the Eurozone.

Indeed, what was forecast as a sharp energy recession just three months ago, is now a shallower, but more prolonged energy and mortgage shock.

The Bank’s rate decision comes before the government unveils its tax and spending plans under new Prime Minister Rishi Sunak at the Autumn Statement on 17 November.

It is the first interest rate meeting since former Prime Minister Liz Truss and former Chancellor Kwasi Kwarteng unveiled their controversial mini-Budget in September.

Their plans for £45bn worth of unfunded tax cuts – much of which have been reversed – sent the value of the pound tumbling and sparked market turmoil, forcing the Bank of England to step in to restore calm.

On Thursday, the pound slumped 2% against the dollar and the cost of government borrowing rose in response to the Bank’s warnings.

Reports /TrainViral/

The prospective new owner of Royal Mail has said he will not walk away from the requirement to deliver letters throughout the UK six days a week, as long as he is running the service.

“As long as I’m alive, I completely exclude this,” Czech billionaire Daniel Kretinsky told the BBC.

Mr Kretinsky has had a £3.6bn offer for Royal Mail accepted by its board.

Shareholders are expected to approve the deal in the coming months, but the government also has a say over whether it goes ahead.

Currently the Universal Service Obligation (USO) requires Royal Mail to deliver letters six days a week throughout the country for the same price. But questions have been raised over whether the service could be reduced in the future.

In an exclusive interview with the BBC, Mr Kretinsky also said he would be willing to share profits with employees, if given the go-ahead to buy the group.

However, he appeared to reject the idea of employees having a stake in Royal Mail, which unions have called for in exchange for their support.

The Royal Mail board agreed a £3.6bn takeover offer from Mr Kretinsky in May for the 500-year-old organisation, which employs more than 150,000 people. Including assumed debts, the offer is worth £5bn.

But because Royal Mail is a nationally important company, the government has the power to scrutinise and potentially block the deal.

As well as keeping the new government on side, Mr Kretinsky also faces the task of convincing postal unions that the proposed deal will benefit employees.

The USO is a potential sticking point for both the government and unions.

Royal Mail is required by law to deliver letters six days a week and parcels five days a week to every address in the UK for a fixed price.

How well this has actually been working in practice is a different matter. Ten years ago, 92% of first class post arrived on time. By the end of last year it was down to 74%, according to the regulator Ofcom.

Last year the regulator fined Royal Mail £5.6m for failing to meet its delivery targets.

Royal Mail has been pushing for this obligation to be watered down. It wants to cut second class letter deliveries to every other weekday, saying this will save £300m, and lead to “fewer than 1,000” voluntary redundancies.

‘Unconditional commitment’

Mr Kretinsky has committed in writing to honouring the USO, but only for five years.

And after that, in theory, the new owners could just walk away from it.

However, Mr Kretinsky told the BBC: “As long as I’m alive, I completely exclude this, and I’m sure that anybody that would be my successor would absolutely understand this.

“I say this as an absolutely clear, unconditional commitment: Royal Mail is going to be the provider of Universal Service Obligation in the UK, I would say forever, as long as the service is going to be needed, and as long as we are going to be around.”

Mr Kretinsky added that the written five-year commitment was “the longest commitment that has ever been offered in a situation like this”.

Another potential stumbling block for the deal, however, is how the company will be structured.

Unions would like to see the company renationalised, but Dave Ward, general secretary of the Communication Workers Union (CWU), told the BBC that would be “difficult in the current political and economic environment”.

Instead, what the CWU is pushing for is “a different model of ownership” – that is, where the employees part-own the business.

To get its support for the takeover, the union wants employees to share ownership of the company, along with other concessions including board representation for workers.

It says profit sharing is “not going to be enough to deliver our support and the support of the workforce”.

If the union doesn’t get what it wants, it won’t rule out industrial action, Mr Ward said. Its members went on strike in 2022 and 2023.

Although Mr Kretinsky said he is “very open” to profit sharing, he is not in favour of shared ownership.

“I don’t think the ownership stake is the right model,” he said. “The logic is: share of profit, yes, [but an] ownership structure creates a lot of complexity.

“For instance, what happens if the employee leaves? He has shares, he is leaving, he is not working for the company, he [still] needs remunerating.”

Mr Kretinsky said he didn’t want to create “some anonymous structure” but instead “remunerate the people who are working for the company, and creating value for the company”.

The union is also concerned about job losses and changes to the terms and conditions of postal workers’ contracts.

Mr Kretinsky has guaranteed no compulsory redundancies or changes in terms and conditions but only until 2025.

“If we are more successful, and we have more parcels to be delivered, we need not less people, but we need more people,” he said. “So really, job cuts are not part of our plan at all.”

He said if the management, union and employees work together, “we will be successful”.

Another concern is the potential break-up of the business.

The profit for Royal Mail’s parent company last year was entirely generated by its German and Canadian logistics and parcels business, GLS. Royal Mail itself made a loss.

Mr Kretinsky has promised not to split off GLS or load the parent company with excessive debt, although borrowings will rise if the deal goes through.

But he has a way to go to convince the CWU.

“I can’t think of any other country in the world that would just just hand over its entire postal service to an overseas equity investor,” Mr Ward of the CWU said.

However, Mr Kretinsky said that the postal unions “do understand that we are on the same ship, and that we need this ship to be successful, and that if we are there, we don’t have any real problems to deal with, because the sky is blue, and it’s blue for everybody.”

The union cannot stop this deal but the government can block it under the National Security and Investment Act.

Business Secretary Jonathan Reynolds has said he will scrutinise the assurances and guarantees given and called on Mr Kretinsky to work constructively with the unions.

Mr Kretinsky may say that he and the unions are ultimately on the same ship but, as things stand, they are not on the same page.

Who is Daniel Kretinsky?

Daniel Kretinsky started his career as a lawyer in his hometown of Brno, before moving to Prague.

He then made serious money in Central and Eastern European energy interests.

This includes Eustream, which transports Russian gas via pipelines that run through Ukraine, the Czech Republic and Slovakia.

He then diversified into other investments, including an almost 10% stake in UK supermarket chain Sainsbury’s and a 27% share in Premier League club West Ham United.

The Czech businessman is worth about £6bn, according to reports.

Father of five blasted for leashing kids, gives them odd nickname

This heartwarming prom story goes viral again and we all understand why

Simon Cowell Won’t Leave Son His $600 M Fortune; Says If He or Future Children Wants to “Start a Business … I’ll Invest. They Aren’t Getting Trusts”

Five wedding outfits for just £29!

Mikhail Gorbachev changed history

Tracking the war with Russia

-

Fashion2 years ago

Fashion2 years agoFive wedding outfits for just £29!

-

Politics2 years ago

Politics2 years agoMikhail Gorbachev changed history

-

Politics2 years ago

Politics2 years agoTracking the war with Russia

-

Everything About Youtube2 years ago

Everything About Youtube2 years agoThe Twitter Artist who makes a Fortune off YouTube Thumbnails while Studying.

-

Fashion2 years ago

Fashion2 years agoOn presents first ever shoe made from carbon

-

Politics2 years ago

Politics2 years agoCharles is announced to be the new King

-

Everything About Youtube2 years ago

Everything About Youtube2 years agoEveryone knows YouTube, but not how it works.

-

Tech2 years ago

Tech2 years agoThe rise of the AI artists stirs debate