Business

Investors calm as Sunak wins race for minister

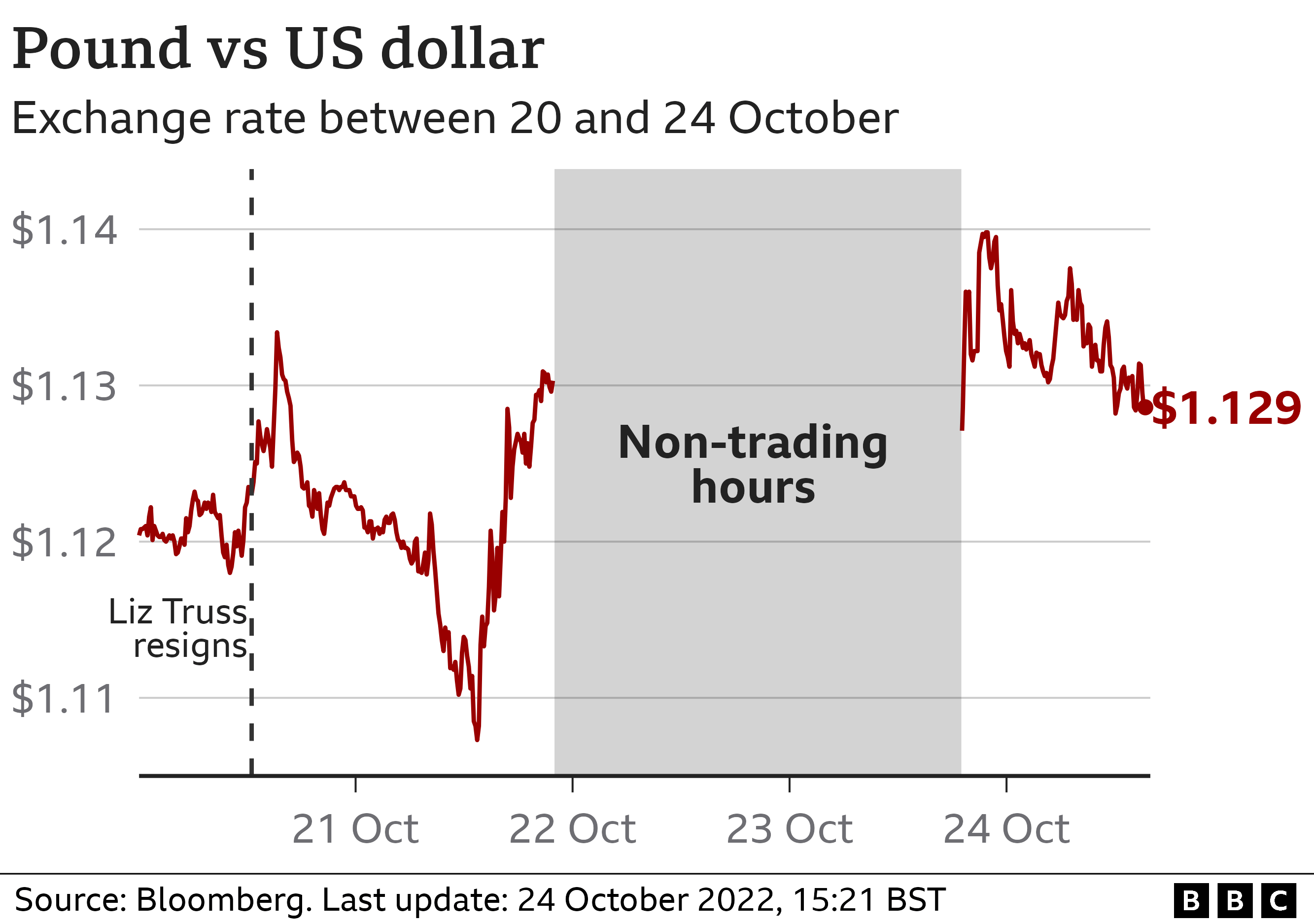

Financial markets have reacted calmly as it emerged that Rishi Sunak is set to be the UK’s next prime minister.

The pound was broadly unchanged against the dollar on Monday afternoon and government borrowing costs stayed lower after Commons leader Penny Mordaunt dropped out of the leadership race.

Earlier in the day, the pound had risen close to $1.14 against the dollar before falling back.

Former PM Boris Johnson withdrew from of the contest on Sunday.

Last month, sterling plunged to a record low against the dollar and government borrowing costs rose sharply in the aftermath of outgoing Prime Minister Liz Truss’s mini-budget.

Investors were spooked after then-Chancellor Kwasi Kwarteng promised major tax cuts without saying how they would be paid for – something Mr Sunak warned about during this summer’s Tory leadership contest.

Last week, new Chancellor Jeremy Hunt withdrew almost all of Ms Truss’s tax cuts in a bid to stabilise the financial markets but they have remained jittery.

On Friday, the pound fell as low as $1.11 and government borrowing costs rose amid continued political uncertainty and fresh warnings about the UK economy.

On Monday, government borrowing costs fell, with the interest rate – or yield – on bonds due to be repaid in 30 years’ time dropping to 3.8%. The rate had hit 5.17% on 28 September after the mini-budget and a subsequent pledge by Mr Kwarteng to announce more tax cuts, prompting interventions by the Bank of England.

Mr Hunt – who is backing Mr Sunak – is scheduled to set out the government’s economic plan for taxes and spending on 31 October.

He has warned the government is facing “decisions of eye-watering difficulty”.

On Monday, the deputy governor for markets and banking at the Bank of England, Sir Dave Ramsden, said the central bank was “engaging” with the Treasury on the upcoming economic plan.

This was after the Bank was not consulted over the mini-Budget.

Sir Dave also told MPs on the Treasury Committee that the recent improvement in gilt yields – the effective interest rates on government borrowing – had shown that “credibility is returning to British economic policy”.

Shevaun Haviland, director general of the British Chambers of Commerce, cautioned that the country “cannot afford to see any more flip-flopping on policies”.

Reacting to the announcement of the new PM, Ms Haviland said: “The political and economic uncertainty of the past few months has been hugely damaging to British business confidence and must now come to an end.

“The new PM must be a steady hand on the tiller to see the economy through the challenging conditions ahead.

“This means setting out fully costed plans to deal with the big issues facing businesses; soaring energy bills, labour shortages, spiralling inflation, and climbing interest rates. ”

‘Sick man of Europe’

Earlier on Monday, financier and long-term Tory supporter Guy Hands said the Conservative Party was not fit to run the country and risked having to ask the International Monetary Fund (IMF) for a bailout.

“I think it’s got to move on from fighting its own internal wars and actually focus on what needs to be done in economy, and admitting some of the mistakes they’ve made in the last six years which have frankly put this country on a path to be the sick man of Europe,” said Mr Hands.

He warned that the UK was headed for higher taxes, reduced public services and higher interest rates which would “eventually” lead to a bailout from the IMF “like we were in the 70s”.

At the weekend, a former governor Bank of England warned that the UK is facing a “more difficult” era of austerity than the one after the 2008 financial crisis in order to stabilise the economy.

Lord Mervyn King said the average person could face “significantly higher taxes” to fund public spending.

The UK is also borrowing billions of pounds to limit energy bill rises for households and businesses.

Borrowing – the difference between spending and tax income – was £20bn in September, up £2.2bn from a year earlier, the Office for National Statistics said.

It was the second highest September borrowing since monthly records began in 1993.

The Institute for Fiscal Studies think tank predicted borrowing this year could reach £194bn, almost double the figure previously forecast by The Office For Budget Responsibility.

Reports /TrainViral/