Business

The ships with gas waiting off Europe’s coast

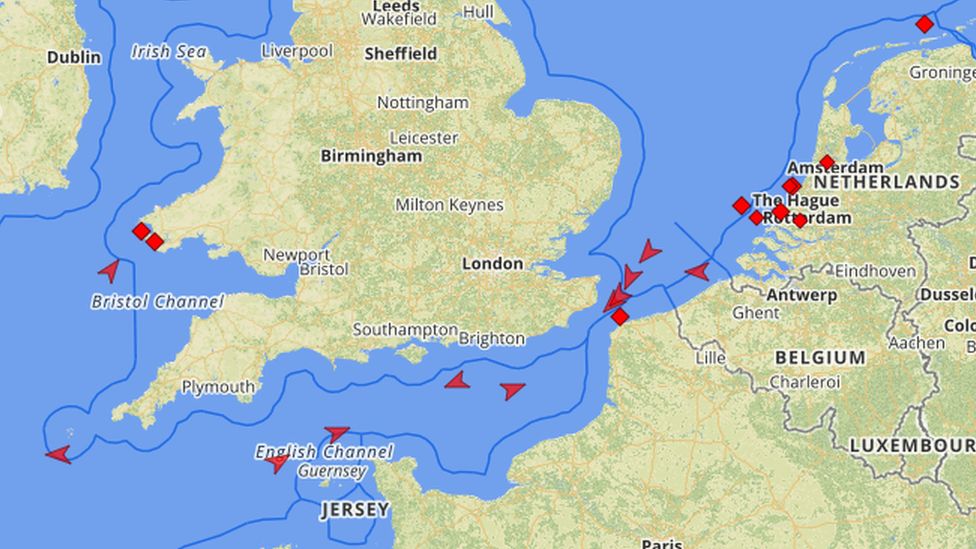

The huge tankers are waiting. Off the coasts of Spain, Portugal, the UK and other European nations lie dozens of giant ships packed full of liquefied natural gas (LNG).

Cooled to roughly -160C for transportation, the fossil fuel is in very high demand. Yet the ships remain at sea with their prized cargo.

After invading Ukraine in February, Russia curtailed gas supplies to Europe, sparking an energy crisis that sent the price of gas soaring. That led to fears of energy shortages and eye-watering bills for consumers.

“It’s built up for about, I would say, five to six weeks,” says Augustin Prate, vice president of energy and commodity markets at Kayrros, one of many observers who has watched the situation unfold.

He and colleagues track ships via AIS (Automatic Identification System) signals, which are broadcast by vessels to receivers, including on satellites.

“Clearly it’s a big story,” he says.

So why are ships loaded with LNG just hanging around Europe, exactly? The answer, as you might have guessed, is a little complicated.

Someone else who has watched the accumulation of vessels is Fraser Carson, a research analyst at Wood Mackenzie. This month, he counted 268 LNG ships on the water worldwide – noticeably above the one-year average of 241. Of those currently at sea, 51 are in the vicinity of Europe.

He explains that European nations plunged into a gas-buying spree over the summer that aimed to fill onshore storage tanks with gas. This was to ensure that heaps of fuel would be available to cover energy needs this winter.

The original target was to fill storage facilities to 80% of their total capacity by 1 November. That target has been met, and exceeded, far ahead of schedule. The latest data suggests storage is now at nearly 95% in total.

Imported LNG has played a key role in getting Europe to this point.

But as LNG continues to be brought ashore, demand for facilities that heat the liquid and turn it back into gas remains high. There aren’t very many such plants in Europe, partly because the continent has long relied on gas delivered via pipelines from Russia instead.

So that’s one reason why LNG ships are waiting around – some are queuing for access to regasification terminals. In the meantime, Germany and the Netherlands have invested in new regasification facilities. Some, rapidly built using converted LNG ships pinned to docksides, are expected to become operational within months.

On top of this bottleneck, less gas is getting used up in Europe than it otherwise might at present because the weather has been very mild well into October.

Plus, as Antoine Halff, co-founder of Kayrros notes, industrial activities that rely on gas have relaxed. This is something he and his colleagues track by scouring satellite images of factories.

“There’s been a very dramatic reduction in cement and steel production in Europe,” he says.

It all means that a market situation called contango has emerged for LNG, says Mr Carson. That is, when the future price of a commodity is higher than today’s price.

“You would get a higher price for a delivery for January than you would in November,” he explains.

Michelle Wiese Bockmann, markets editor and analyst at the shipping journal Lloyd’s List, says that just by waiting to deliver in December rather than November, the difference in profit could be in the order of tens of millions of dollars per shipment.

While it is possible that buyers elsewhere in the world could snap up the cargoes of some waiting ships, meaning they might leave and head to Asia, for example, it may yet benefit Europe to have a glut of LNG literally floating around.

Some observers say having the ships wait around is partly a good thing – you want the gas to be available when you need it.

The only spanner in the works is the sobering sums involved. Feverish demand for gas means that countries have already paid extraordinary amounts to secure it.

Germany spent 49.5bn euros (£43.25bn) on imports between January and August, according to the Reuters news agency. That’s compared to 17.1bn euros during the same period in 2021.

This is “market forces” at work, says Ms Bockmann. But she emphasises that European nations are “in the best possible position that they could be [in], given the geopolitical situation”.

Mr Carson agrees, adding: “In terms of what can actually be done at the moment, the market has responded appropriately.”

The real question is what happens next. With gas secured for the coming weeks at least, the price of the commodity in Europe has begun to fall.

Benchmark gas prices in Europe have fallen dramatically since August, but are still more than twice the price they were this time last year.

However, further disruptions to supply and very cold winter months could potentially change the picture yet again.

There’s also the global situation to consider. Heightened demand for LNG imports in Europe has boosted competition for gas around the world. Countries such as Pakistan and Bangladesh that rely on LNG, but which have less financial leverage in the market, have been stung by the current situation.

In general, some LNG that might traditionally have gone to Asia has this year sailed to Europe. It has effectively been “a huge game of musical chairs”, says Mr Halff.

But some Asian nations, notably China, Japan and South Korea, which also use a lot of LNG, will likely seek significant imports in the colder months, potentially fuelling competition between continents.

For Corey Grindal, chief operating officer and head of worldwide trading at LNG producer Cheniere, what’s happening in the LNG market is “a very short-term phenomenon”.

Diversification of energy supplies in Europe should ease things in the coming years.

He adds that the vast majority of his firm’s LNG output this year has already been sold and that Cheniere’s production should rise from 45 million tonnes to 55 million tonnes by around 2026.

The current bonanza over gas has concerned some who argue that pivoting to renewables would be better for the planet and possibly more reliable.

“Renewable deployments is great. I am [all] for doing the right thing for the planet that we live on,” says Mr Grindal.

However, he argues that the need for gas to heat people’s homes and generate electricity is immediate. “We need it today,” he says.

What happens tomorrow depends, in varying degrees, on the war in Ukraine, the weather, the rise of renewables, global demand for gas – and hundreds of ships full of LNG sailing either east or west.

Reports /TrainViral/