Business

What happened to the UK economy?

It’s just over a week since the new Chancellor, Kwasi Kwarteng, presented his tax-cutting mini-budget. His aim was to kickstart economic growth. But it seems to have kickstarted a crisis of confidence, a jump in mortgage rates, and calls for a complete U-turn.

So what just happened? Here’s a quick run-through of a dramatic week for the UK economy, told by the people who lived it.

On Monday London currency trader Jordan Rochester woke up at 06:00, rolled over to check his phone and saw the pound had fallen to its lowest level on record: $1.03.

The questions came flooding in: How far can it fall? Will the Bank of England do an emergency interest rate hike? What will the government do to save the pound?

“There was a mad dash to answer these important questions to clients,” he says.

Luckily for him, for the last few months, he has been betting against the pound, expecting it to fall.

“It’s possibly been the best trade of my career, but perhaps also the least enjoyable,” he adds. “After all, nobody wants a recession.”

A weaker currency suggests investors’ faith in a country’s economic prospects is wavering.

Although it came at a time when the dollar was already strengthening, the pound was knocked further by a mini-budget that outlined surprise tax cuts and a huge package of help with energy bills, but didn’t spell out where the extra money would come from to pay for it.

It didn’t come with any independent analysis of how the numbers added up, which made things worse.

The fall in sterling immediately made things tougher for Mike Walley, owner of toy retailer Everything Dinosaur in Cheshire. He had a $42,000 bill to pay for imported stock.

“Had we made that payment last week it would have been about £35,000,” he said on Monday. “Now, because of the pound situation, it is getting on towards £39,000 that we have to pay.”

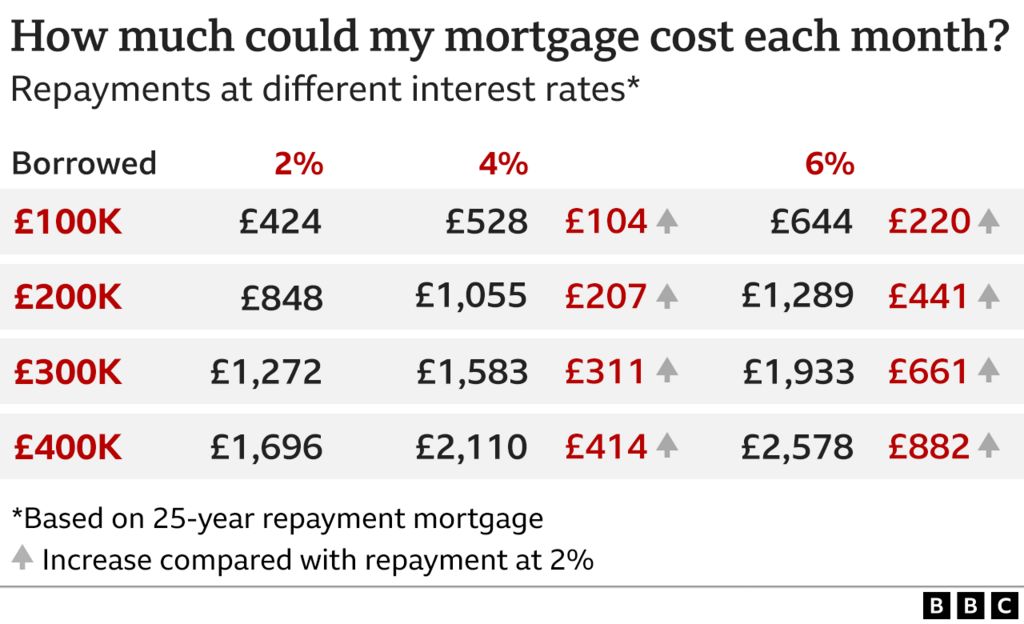

By Tuesday there were expectations that the Bank of England would have to raise interest rates to counter the extra spending in the mini-budget.

That sent the phones ringing off the hooks for mortgage brokers like Andrew Montlake at Coreco Partners.

“The beginning of the week was absolutely crazy, a whirlwind of activity and confusion,” he says.

His staff worked around the clock to help clients tie down deals before lenders pulled their products or replaced them with more expensive ones.

By the end of the week there were 40% fewer products available than before the mini-budget.

“If we spoke to a client at nine in the morning and quoted them a rate, we had to phone back two hours later and say: ‘It’s going in the next hour. You need to make a quick decision if you want it,'” he says.

People about to come off fixed rates are facing huge jumps in their monthly payments, he adds.

That’s what is worrying Steve Kendrick, 51, from Cardiff, who feels as though he is heading for disaster.

“If interest rates rise as suggested, I will lose my home,” he says. “It astounds me that after everybody worked so hard through Covid, we have to go through this. It’s like being stabbed in the back.”

The government’s strategy is likely to increase inequality and add to pressures pushing up day-to-day prices, the International Monetary Fund pointed out. It was an unusually outspoken statement from the Fund, which often bails out countries who are struggling financially.

On Wednesday the cost of government borrowing was rising to levels many economists thought were concerning.

It was a “kneejerk” lack of confidence, explains Lucy Coutts, investment director at JM Finn.

She invests in government bonds, which she says are usually like sloths – they’re low risk, they don’t move, because lending to the UK is considered an ultra-safe bet. But some bonds fell by 20% in two days.

“These are seismic moves in very sleepy instruments,” she says.

She was on the phone to a client when she saw news that the Bank of England had stepped in to support bond values by promising to buy up £65bn of them over the next few weeks.

“I thought, that’s really serious,” she says. But it only became clear later that the action had been absolutely necessary to avoid a panic in the pension market.

Thanks in part to that intervention, by Thursday things had begun to settle down.

Liz Truss and Kwasi Kwarteng took to the airwaves to defend their package of measures, saying they would stick to their plan despite the criticism.

The prime minister said the strategy would get the economy growing and deal with inflation – and that she was not afraid to take controversial and difficult decisions.

Chancellor Kwasi Kwarteng defended his mini-budget measures, saying they were “absolutely essential” in “delivering much better growth outcomes for people”.

In a WhatsApp message to fellow Conservative MPs he said: “The path we were on was unsustainable – we couldn’t simply continue to raise taxes. However I totally understand the need to be credible with markets. We will show markets our plan is sound, credible and will work to drive growth.”

Lucy Coutts says she found it a “massive reassurance” that the prime minister had confirmed her commitment to an independent Bank of England. Government bonds recovered some of their losses.

But share prices fell sharply on the UK stock market.

And Labour, who, according to one poll have taken a 33-point lead over the Conservatives, said parliament should be recalled so the “kamikaze” budget could be reversed.

By Friday mortgage lenders were returning with new product offers, although the rates had shifted up a percentage point or two and brokers warned the market was in “very choppy waters still”.

Shares had made up some lost ground too.

But after meeting the Office for Budget Responsibility (OBR) in the morning, the prime minister and chancellor still said there would be no official independent analysis of their plans from the economic watchdog, until the next full budget, scheduled for 23 November.

Lucy Coutts said the government’s credibility remained in question until they could provide an explanation of how spending would be paid for and debt would be managed over the longer term. “Their working out, that’s what we want.”

Sterling was almost back at pre-mini-budget levels by the end of Friday – good news for Mike Walley who has already managed to save a few hundred pounds by holding off on one of his dollar payments until the end of the week.

He is still worried about “turbulent times” in the run-up to Christmas, though.

“We understand this is all about going for growth. But what businesses really need is stability.”

Reports /TrainViral/